How Long Does Mortgage Pre-Approval Take?

Unlock the secrets to a speedy mortgage pre-approval! Learn what impacts the timeline and avoid common pitfalls. Get pre-approved faster and find your dream home sooner! Mortgage Pre-Approval is key!

Securing a mortgage pre-approval is a critical step in the home-buying process. It gives you a clear picture of how much you can borrow, strengthens your offer when you find a house, and ultimately saves you time and potential heartache. But how long does this vital process actually take? The answer, unfortunately, isn’t a simple number. Several factors influence the timeline, and understanding these nuances is key to navigating the process efficiently.

Understanding the Mortgage Pre-Approval Process

The pre-approval process involves a lender assessing your financial situation to determine your borrowing capacity. This isn’t just a quick glance at your credit score; it’s a thorough examination of your income, debts, assets, and credit history. Lenders want to ensure you’re a responsible borrower who can comfortably manage monthly mortgage payments.

Step 1: Initial Application and Documentation

The first step typically involves completing a mortgage application form. This form will request extensive personal and financial information, including your income, employment history, assets, debts, and credit history. You’ll also need to provide supporting documentation, such as pay stubs, tax returns, bank statements, and W-2 forms. Gathering all this information upfront can significantly speed up the process. Be prepared for a potentially lengthy list of requirements.

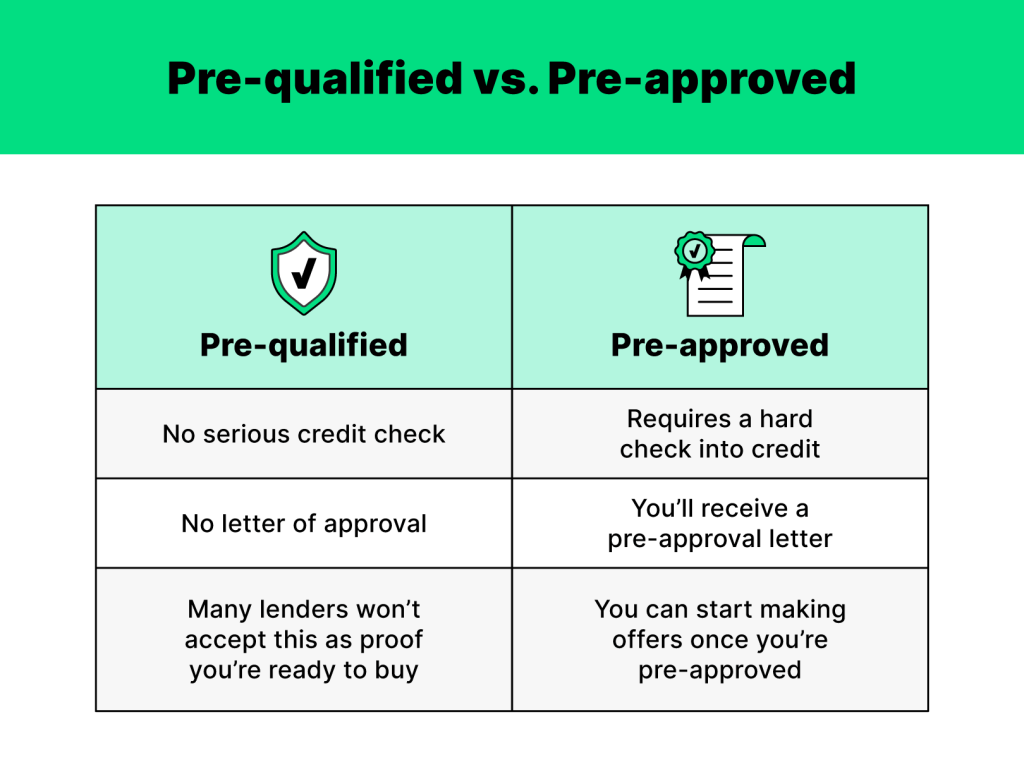

Step 2: Credit Report Review and Appraisal

Once your application is submitted, the lender will pull your credit report. This is a crucial part of the process as it reveals your creditworthiness. A high credit score generally leads to a quicker and smoother pre-approval. Following the credit check, the lender may also order an appraisal of the property you intend to purchase, though this is usually done after you’ve found a home and made an offer.

Step 3: Underwriting and Final Approval

After reviewing your financial documentation and credit report, the lender’s underwriters will analyze your application in detail. They’ll verify your income, employment, and assets. This stage can be time-consuming, as underwriters meticulously examine every detail to assess the risk involved in lending you money. Any inconsistencies or missing information can delay the process. A thorough and accurate application is therefore paramount.

Factors Affecting Pre-Approval Timelines

The time it takes to get pre-approved for a mortgage can vary significantly depending on several factors. These factors can range from your personal financial situation to the lender’s efficiency and the complexity of your application;

Your Financial Situation and Documentation

The completeness and accuracy of your financial documents significantly impact the pre-approval timeline. Missing documents or inconsistencies in your information can cause delays as the lender requests clarification or additional documentation. Organize your financial records meticulously to avoid unnecessary delays.

The Lender’s Processing Speed

Different lenders have different processing speeds. Some lenders are known for their efficient and streamlined processes, while others may take longer. Research and choose a lender with a reputation for timely processing to expedite the pre-approval process. Reading online reviews can often provide insights into a lender’s efficiency.

The Complexity of Your Application

The complexity of your financial situation can also influence the pre-approval timeline. For example, self-employment, complex income streams, or a less-than-perfect credit history can prolong the process. Be prepared to provide more detailed documentation to support your application if your financial circumstances are complex.

Time of Year

Interestingly, the time of year can also play a role. The mortgage industry experiences peak seasons, often during the spring and summer months when the housing market is most active. During these busy periods, lenders may experience higher volumes of applications, potentially leading to longer processing times.

Typical Timeframes and What to Expect

While there’s no single definitive answer to how long mortgage pre-approval takes, a reasonable expectation is between one to four weeks. However, this is just an estimate. In some cases, the process might be completed within a week, while in others, it could take several weeks or even longer.

- Ideal Scenario (1-2 weeks): This typically involves a straightforward application with complete and accurate documentation, a strong credit score, and a lender with efficient processing.

- Average Scenario (2-3 weeks): This is a common timeframe, accounting for potential minor delays in gathering documentation or lender processing.

- Lengthier Scenario (3-4+ weeks): This could be due to complexities in the applicant’s financial situation, incomplete documentation, or a less efficient lender.

Tips for Expediting the Pre-Approval Process

Several steps can help you expedite the pre-approval process and minimize potential delays. Proactive preparation and clear communication are key to a smooth and efficient experience.

- Gather all necessary documents in advance. This includes pay stubs, tax returns, bank statements, W-2 forms, and any other relevant financial documents.

- Check your credit report for errors. Addressing any errors before applying can prevent delays.

- Choose a reputable lender. Research lenders and choose one with a good reputation for timely processing.

- Be responsive to lender requests. Promptly provide any additional information or documentation requested by the lender.

- Ask questions. Don’t hesitate to contact your lender if you have any questions or concerns throughout the process.

The Importance of Pre-Approval

Securing mortgage pre-approval offers numerous advantages. It gives you a realistic budget, strengthens your offer when you find your dream home, and demonstrates your seriousness to sellers. It can also save you significant time and effort by preventing you from falling in love with homes you can’t actually afford.

Pre-approval provides a crucial advantage in the competitive real estate market. It shows sellers you’re a serious buyer, ready to close the deal. It also saves you from wasted time and emotional energy looking at homes outside your financial reach. The peace of mind that comes with knowing your financial standing is a significant benefit in itself. Knowing your borrowing power allows for a focused and efficient home search, leading to a smoother and less stressful home-buying journey. This proactive approach sets the stage for a successful and fulfilling home ownership experience.